After turning 70, I’ve come to realize that, at least for me, “70 is the new 60” is more myth than reality. In the first half of 2026, I began slowing down by ending my around-the-clock commentary on metals and mining, particularly junior resource stocks and my personal portfolio. Going forward, I will focus on broader macro analysis, with metals and mining included only as part of a wider view of financial markets.

Much of the financial services industry and mainstream financial media remain firmly in the “Don’t Worry, Be Happy” camp. You could throw them off the Empire State Building, and on the way down they would still say, “So far, so good.” Yet the evidence keeps mounting that the greatest financial bubble of all time has already begun to deflate, with the full collapse likely still ahead. Whether it comes in a day, a week, a month, or later, most investors who stay aggressively long will not be able to get out in time.

Many in the business portray their approach as highly sophisticated, built on complex processes or black-box systems that guide them and their clients. My own process, shaped by more than 42 years in and around the financial arena, is far simpler—and it has worked far more often than not.

I ask myself a simple question: if a genie handed me a pile of free money and made me choose between investing it all in my stocks or selling my stocks and keeping the cash, what would I do? If I would hesitate to put that found money into my portfolio, then I must ask why I am keeping my hard-earned money there now.

Simply put, I could not start a U.S. stock market equity portfolio today, even at gunpoint. That does not mean the market must fall sharply tomorrow, but there are too many better alternatives. For me, that means fully applying three golden rules:

1 – Capital preservation over capital appreciation.

2 – Going forward, the winners will be separated from the losers not by how much they make, but by how much they avoid losing.

3 – There is no shame in being a live chicken rather than a dead duck.

Some equity exposure can still be useful, especially for retirees or those nearing retirement. In my view, RILAs—or ETFs that mimic them—fit that role well. Participating in gains while avoiding losses during market declines aligns with my current outlook.

I continue to favor one-year T-Bills, thankfully, as Treasuries have lost money for four consecutive years.

After avoiding much of the major decline in gold, silver, and mining shares, I recently moved back in. While prices could still fall below my re-entry levels, I believe the longer-term upside is far brighter than the remaining downside risk.

I believe the following factors deserve everyone’s attention. They are among the reasons I believe America has entered its most difficult economic, social, and political era. That view is certainly not popular, especially as the country prepares to celebrate its 250th anniversary. But there are only two types of advisors: those who say what they truly believe, and those who say what they think people want to hear because it sells. I will never be part of the latter group.

Retirement and Aging Crisis – So many are going to end up not knowing what hit them.

- Social Security And The Retirement Crisis. From Bad To Worse.

The Retirement Crisis Is Going From Bad To Worst

Retirement And Aging Crisis – From Bad to Worse

The Future Economy – I’m not very optimistic.

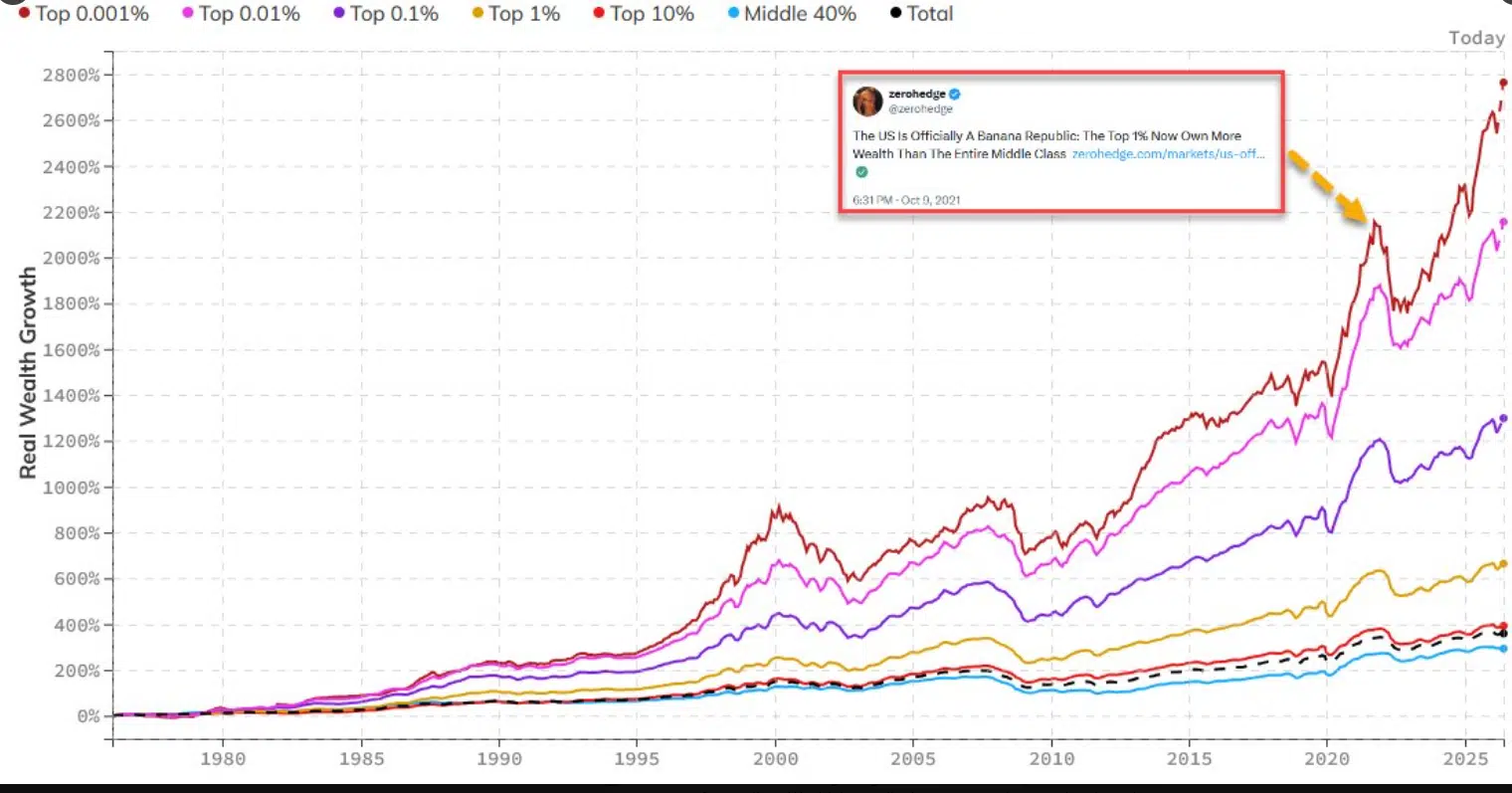

- The US wealth divide has never been bigger. The top 20% of earners now account for ~58% of all personal spending in the US, the highest proportion on record.. At the same time, the bottom 80% account for just ~42%, the lowest on record. America doesn’t fund its own investment anymore. Net national saving has declined to under 1% of GDP, from over 11% in the 1960s.Zero net savings. We now borrow most of what we invest from the rest of the world.

A record 33% of household wealth is now held by Americans that are 70 years of age and older.

U.S. corporations are keeping the largest share of national income since 1950, while the share going to workers hit an all-time low.

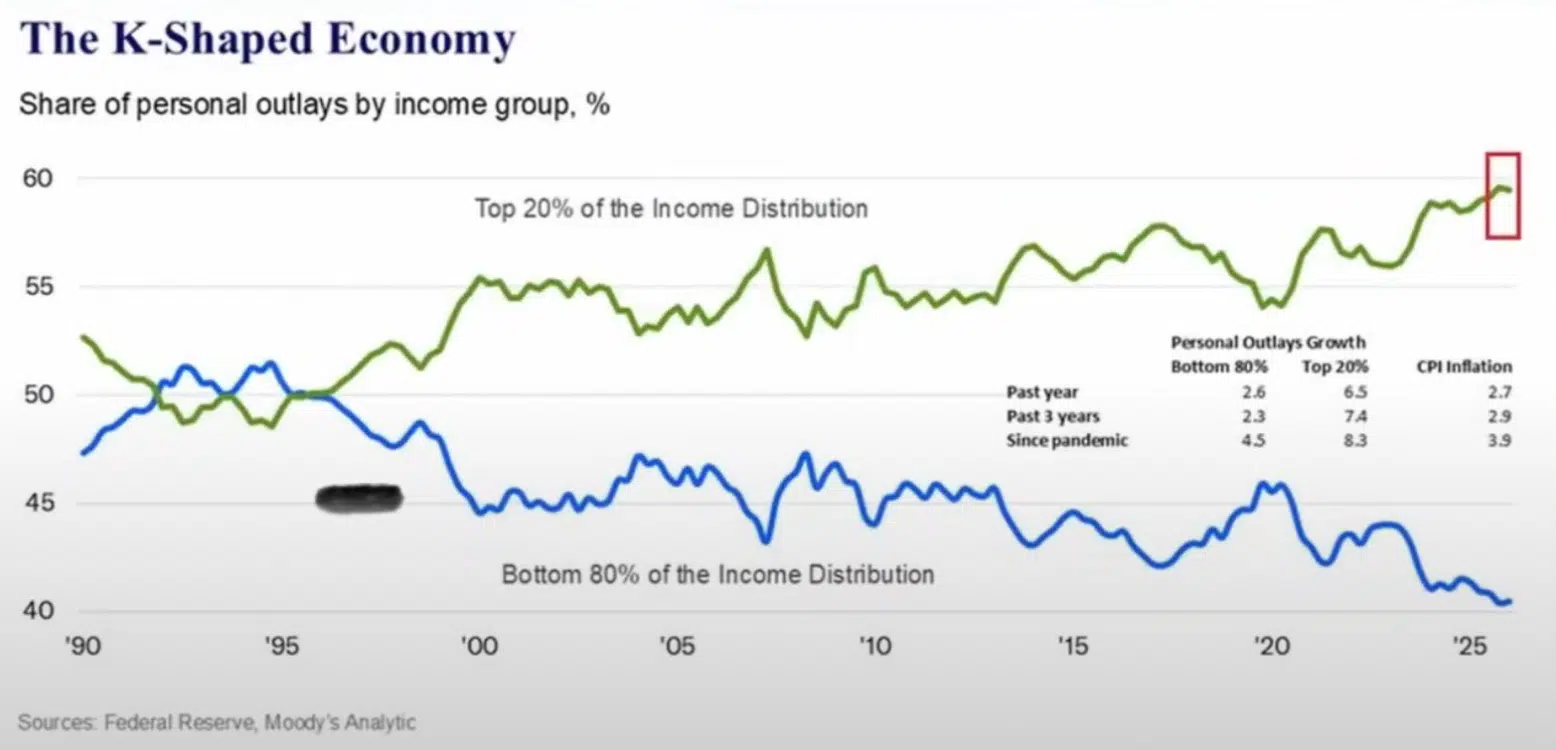

Moody’s chief economist Mark Zandi reports that the top 10% of earners accounted for 49.2% of consumer spending in Q2 2025, up from 36% in the early 1990s, based on Federal Reserve data. The top 20%—those earning over $175,000—handled nearly 60% of outlays in Q1 2026, with their spending rising 6.5% last year while others fell behind inflation. This K-shaped divide, fueled by gains in stocks and real estate, keeps growth strong since consumer spending makes up 70% of GDP, though Zandi warns of risks if the wealthy cut back.

It wasn’t raining when Noah built the Ark. Time is running out to build your own Portfolio Ark.

Peace Be With You – Peter Grandich